Banks often advertise a neat percentage. They rarely explain what that number means to you. The real value is in the yield. The math behind yield is simple.

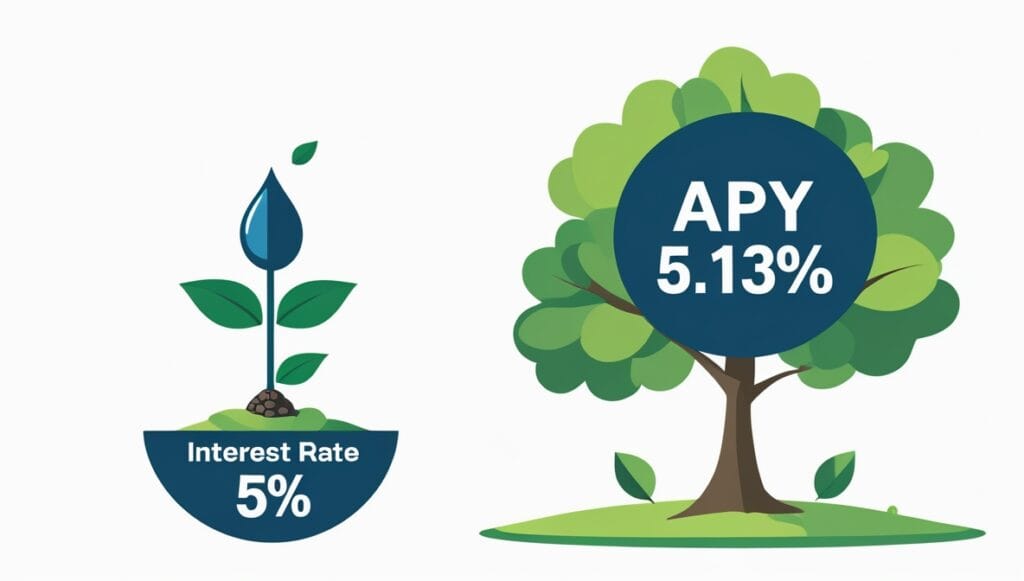

Rate vs APY

When a bank posts “5%,” it may mean one of two things. It might be the nominal interest rate. That is the simple, stated yearly rate. Or it might be the APY. APY stands for Annual Percentage Yield. APY shows the actual percentage you earn in one year after compounding.

Think of the nominal rate as the seed and APY as the full-grown tree. The seed promises growth. APY shows what you actually harvest.

This matters because if two banks show the same seed number but different compounding schedules, APY will differ. The higher APY is the better deal.

How the math actually works

Here is the exact formula banks use. I will write it first, then translate.A=P(1+nr)nt

Now the plain-English version.

P stands for Principal. This is the money you start with.

r stands for the nominal annual rate, expressed as a decimal. For 5 percent, r = 0.05.

n is the compounding frequency. It is how many times per year the bank pays the little interest bonus. Monthly means n = 12. Daily means n = 365.

t is time in years. For 18 months, t = 1.5.

A is the final amount in your account after t years. Interest earned equals A minus P.

Why this formula works. Each time the bank pays interest, that interest joins the principal, and itself earns more interest in the next period. This is compounding. The formula stacks the per-period growth factor (1+r/n) for n times each year and for t years.

To get APY from a nominal rate, set t = 1 and compute:APY=(1+nr)n−1

APY is the effective annual yield. It is what you compare across banks.

Why does daily always beat monthly?

Daily compounding means the bank credits interest each day. Monthly compounding credits interest each month. Daily gives you slightly more interest because you earn interest sooner on the interest you already earned.

Numbers help. Use a $10,000 deposit at a 5.00% nominal rate for one year.

Monthly compounding, n = 12:Amonthly=10,000(1+120.05)12≈10,511.62

Daily compounding, n = 365:Adaily=10,000(1+3650.05)365≈10,512.67

The monthly interest earned is about $511.62. Daily interest earned is about $512.67. The difference for one year and $10,000 is $1.06.

That sounds tiny. Now look at five years with the same starting deposit and nominal rate.

Five years, monthly:A5yr, monthly≈12,833.59

Five years, daily:A5yr, daily≈12,840.03

The five-year difference is about $6.45 on a $10,000 deposit. Still small for $10,000. But scale that to larger amounts and longer terms. For $100,000, the five-year difference is roughly $64.50. For $1,000,000, it is about $645. Do not dismiss small per-dollar differences. Over portfolios and time, they add up.

Also, remember banks may advertise APY already. When they do, the compounding effect is baked into the APY. If they show a nominal rate and do not show APY, ask for both compounding frequency and APY.

The logic you can use in minutes

Step one. Always check APY first. If APY is shown, use it to compare offers directly.

Step two. If only a nominal rate is shown, ask for compounding frequency n. Convert to APY with the formula above.

Step three. Plug your principal P and time t into the compound formula. That gives the exact final balance A.

Step four. If you plan to withdraw early, calculate penalties and subtract them. See the FAQ below.

While every Certificate of Deposit offers a guaranteed, fixed return, not all CDs are the same. Understanding the different types, from standard fixed-rate accounts to flexible or tax-advantaged options, is essential for maximizing your savings strategy. Choose the CD that matches your liquidity needs and financial goals.

Ready to run the numbers? Use our High Yield CD Calculator to project your earnings on any CD term.

Types of Certificates of Deposit

1. Traditional and Jumbo CDs

The Traditional CD is the foundation of the market. You deposit a lump sum for a fixed term (e.g., 1 year, 5 years) and receive a fixed interest rate (APY). The key trade-off for the guaranteed return is limited access to your money; early withdrawal almost always incurs a penalty.

Jumbo CDs: Larger Deposits, Higher Rates

- Jumbo CDs typically require a minimum deposit of $100,000 or more.

- In exchange for this large commitment, banks may offer a *slightly* higher APY than a standard CD with the same term.

- Jumbo CDs are still FDIC-insured, but investors should be aware that the $250,000 limit applies per depositor, per institution.

2. No-Penalty CD (Liquid CD)

A No-Penalty CD offers the best of both worlds: a higher, locked-in rate than a typical savings account, with the flexibility to withdraw your entire principal and earned interest early without penalty.

Key Feature: Liquidity

Withdrawals are generally allowed anytime after the first 6 or 7 days of funding, making this an ideal vehicle for emergency funds or savings goals with flexible timelines.

The trade-off is often a slightly lower APY compared to a rigid Traditional CD.

The Break-Even Math: No-Penalty vs. Standard CD

To calculate if a No-Penalty CD is worth the lower APY, you must find the Effective Yield after a hypothetical withdrawal.

Scenario: > Standard CD: 5.00% APY with a 90-day Early Withdrawal Penalty (EWP).

- No-Penalty CD: 4.50% APY with zero penalty.

If you withdraw after 120 days, the math changes:

- Standard CD Effective Yield: You earn 120 days of interest but lose 90 days to the penalty. You only keep 30 days of earnings.

- No-Penalty CD Effective Yield: You keep the full 120 days of earnings at 4.50%.

The Formula for No-Penalty Earnings:

Compare current No-Penalty CD rates to see if the flexibility is worth the potential difference in APY.

3. Bump-Up and Step-Up CDs

These CDs are designed for environments where interest rates are expected to rise, giving you a hedge against inflation.

Bump-Up CD

Gives the investor a one-time (or limited) option to manually increase their CD rate to a higher rate offered by the bank during the term.

Pro: You choose the best time to increase the rate.

Step-Up CD

The interest rate automatically increases at predetermined intervals (e.g., every 6 or 12 months), regardless of market rates.

Pro: Rate increases are guaranteed and automatic.

Both types usually start with a lower initial APY than a Traditional CD of the same term length.

4. Retirement and Investment CDs

IRA CDs (Tax-Advantaged)

An IRA CD is a standard CD held inside an Individual Retirement Account (IRA), such as a Traditional or Roth. This allows the CD’s interest to grow with tax advantages (tax-deferred or tax-free). They are ideal for retirement savers seeking a guaranteed, low-risk component for their portfolio.

Brokered CDs (Higher Volume)

Brokered CDs are bought through a brokerage firm (like stocks) rather than directly from a bank. This gives investors access to a wider selection of banks and often higher limits. They are used by investors to easily manage multiple CDs across different institutions to keep total balances under the $250,000 FDIC limit at each bank.

Which CD Type is Right for You?

The right choice depends on your timeline and flexibility needs. If you’re confident in locking your money away, go for the highest Traditional APY. If you need a flexible emergency buffer, consider a No-Penalty option.

FAQs

What is the Banker’s Year, 360 vs 365?

Banks sometimes use a 360-day year for interest calculations. That is the Banker’s Year. The formula for daily simple interest becomes Interest=P×r×360d where d is days. For compound interest, daily compounding with n = 360 slightly changes the result. The difference between 360 and 365 for retail CDs is tiny. But for large balances or precise accounting, confirm which convention the bank uses.

Why does my bank statement not match my calculation?

There are three common reasons. First, you may be using a different day-count convention (360 vs 365). Second, the bank may credit interest on different days or use business day adjustments. Third, the bank may compound at a different frequency than you assumed. Always check the account terms for compounding frequency and day-count method.

Does the yield change if I take money out early?

Yes. Early withdrawal penalties can reduce your effective yield. A common penalty is loss of several months of interest. Model it like this. Compute the raw balance A at withdrawal time. Compute the penalty in dollars. Subtract the penalty from A to get net proceeds. Convert net proceeds back to an annualized yield over the actual holding period. Many times, the penalty turns a positive yield into a much lower effective rate. If you might need cash, factor penalties into your decision.

How does APY relate to a nominal rate I see advertised?

APY converts the nominal rate plus compounding into a single number. If you have r and n, solve APY = (1+r/n)n−1. That gives you the effective annual growth.

What is the Rule of 72, and does it apply to CD yields?

The rule of 72 is an approximation for doubling time. Divide 72 by the effective annual return percentage. For an APY of 5%, the doubling time ≈ 72 / 5 = 14.4 years. Use APY, not nominal rate, for the most accurate estimate.

If my principal is large, is compounding frequency more important?

Yes. The dollar-gap grows with principal and time. A small additional APY point matters more on $100,000 than on $1,000.

What is the effect of taxes on CD yield?

Interest from CDs is taxed as ordinary income in the year it is credited or paid, depending on account rules. To compute the after-tax yield, subtract your marginal tax rate from the yield. For example, at a 22% tax rate, a 5% yield reduces to an after-tax yield of about 3.9%.

Final logic and action

The math here is not an obstacle. It is a tool. When you compare two CD offers, the correct steps are simple. Use the APY value when available. If not available, compute APY from the nominal rate and compounding frequency. Plug your numbers into the compound formula. Scale results to your actual principal and term. Factor in taxes and penalties.

If you want to skip manual math, use our calculator. It runs the exact formulas and shows period-by-period results. Try the High Yield CD Calculator to test your exact scenario instantly. All inputs and outputs are handled transparently in line with our Privacy Policy and Terms of Use. Your data stays private, and the math stays exact.